On April 9th, the SEC’s Division of Examinations issued a “Risk Alert” regarding three types of financial firms – investment advisers, registered investment companies, and private funds – that offer Environmental, Social & Governance (“ESG”) products and services. The Examinations Division is prioritizing review of ESG practices in response to the rapidly growing demand by investors that their asset managers address climate change and other environmental issues and the dizzying array of actions taken by asset management and advisory firms in response to this investor demand.

Last month, Vanguard and Blackrock, two of the world’s two largest asset managers with massive investments in fossil fuel companies and forest-destroying agribusinesses, joined a group of investment firms in a pledge to cut the net greenhouse-gas (GHG) emissions of their portfolios to zero by mid-century. Together, this group of firms manages more than $28.8 trillion (US) of assets. If this pledge is real – that is, if it is accompanied by meaningful and timely action – it is truly an historic one. The steady loss of the habitability of the earth can be averted only if financial institutions stop worsening the climate crisis and instead reorient investments toward carbon pollution reduction and resilience to extreme weather events. Investors, especially everyday retail investors, will need the SEC’s help in assessing whether and how financial firms’ products and services square with their recent “net zero” pledges.

To date, no consensus on standards or methodologies has been reached on what constitutes an acceptable plan for net zero GHG emissions by mid-century. According to the Examinations Division, this absence of a consensus framework plagues the entire suite of ESG practices, and this vacuum creates an opening for financial firms to engage in misleading conduct regarding their performance.

The Examinations Division found a variety of problems regarding ESG practices. With regard to investing processes, they found, among other things, that in some cases “portfolio management practices were inconsistent with disclosures about ESG approaches” and there are “inadequate controls to ensure that ESG-related disclosures and marketing are consistent with the firm’s practices.”

Division staff found two types of potentially misleading statements or omissions:

- Proxy voting may have been inconsistent with advisers’ stated approaches

- Unsubstantiated or otherwise potentially misleading claims regarding ESG approaches

Other research confirms that proxy voting by financial firms has contradicted stated approaches. In a 2019 study, researchers at Majority Action evaluated 28 climate resolutions at companies where Vanguard and Blackrock were top common stock shareholders and found that at least 16 of these resolutions would have passed if Vanguard and Blackrock had not voted against them. Most of these defeated resolutions called for climate risk disclosure, a principle which both firms have promoted in their public communications.

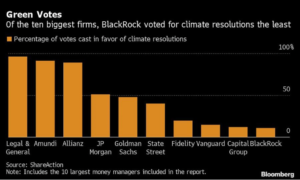

Similarly, research by ShareAction on shareholder meetings held in the 12 months through August 2020 shows that BlackRock and Vanguard were among the least supportive of climate resolutions, voting in favor of them just 11% and 15% of the time.

Are financial firms “greenwashing” when they assure shareholders and the public that they are leaders on climate risk but then quietly take action to exacerbate this risk? Very likely. Is this greenwashing sufficiently deceptive to constitute actionable fraud under the Securities Exchange Act? This is unclear. Fortunately, the SEC is moving quickly to address confusion about what kind of disclosure about climate risk management practices is required:

- In February, Acting Chair Allison Herren Lee instructed the Division of Corporation Finance to assess how the SEC can ensure compliance with disclosure rules on the books as well as update existing guidance on climate risk disclosure. She indicated that this assessment would help put the SEC on a path to developing a more comprehensive framework that produces consistent, comparable, and reliable climate-related disclosures.

- In March, Acting Chair Lee launched a Climate and ESG Task Force in the SEC’s Division of Enforcement, charging with coordinating the efforts of the Office of the Whistleblower and other parts of the agency to address “emerging disclosure gaps” relating to climate change and ESG.

- Also in March, Acting Chair Lee asked SEC staff to evaluate climate risk disclosure rules and invited the public to share data and perspectives on 15 questions that will be considered as part of this evaluation. Responses to this invitation for comments are due June 13. NWC and its allies will be submitting detailed answers and recommendations.

The SEC must be encouraged to keep moving expeditiously on both climate risk rulemaking as well as whistleblower-assisted enforcement of existing anti-fraud rules when material climate risks are concealed. The planet is facing a climate emergency, and all public companies have a legal and ethical duty to be truthful with their investors and the public about whether they are playing a constructive role in the rescue. With this critically-needed information, climate-aware investors can shift their investments and regulators can address the threats to the financial system posed by climate risk.